2QFY2019 Result Update | Dairy Products

November 6, 2018

Parag Milk Foods

BUY

CMP

`256

Performance Update

Target Price

`330

Y/E March (` cr)

Q2FY19

Q2FY18

% yoy

Q1FY19

% qoq

Investment Period

12 Months

Net sales

573

505

13.7%

549

4.4%

EBITDA

58

50

16.3%

60

-2.7%

EBITDA margin (%)

Stock Info

10.1%

9.9%

10.9%

Adjusted PAT

30

25

22.2%

28

7.6%

Sector

Dairy Products

Market Cap (` cr)

2,153

For Q2FY2019, Parag Milk Foods (PARAG) posted decent performance with

Net Debt (` cr)

214

14%/22% yoy growth in revenue/ PAT led by 23 bps expansion in margin. The

Beta

1.1

company has maintained its revenue target of `2700+ crore for FY2020 backed

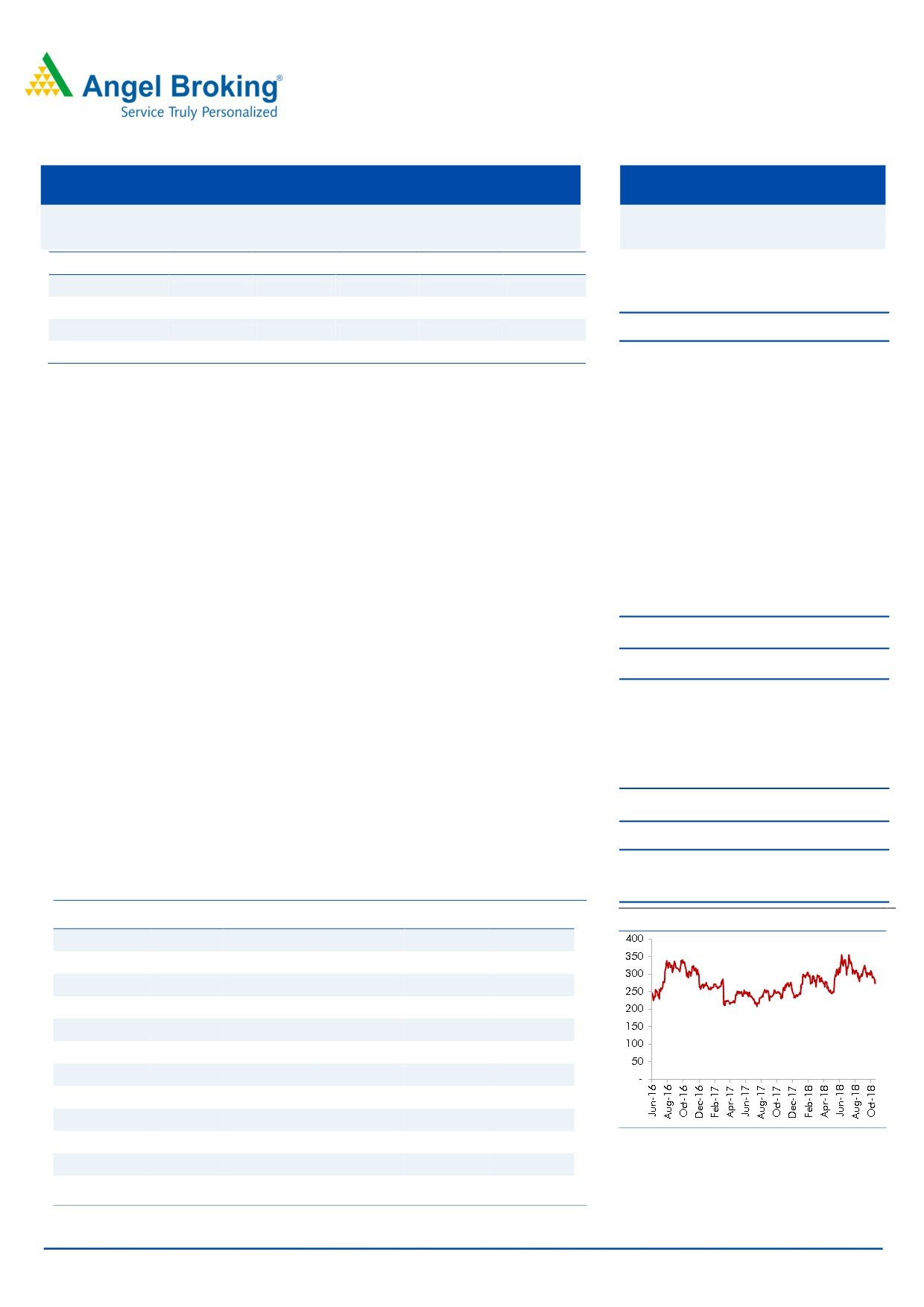

52 Week High / Low

414/220

by widening distribution network and product portfolio.

Avg. Daily Volume

1,38,424

Revenue rose 14%: Q2’s top-line growth was led by growth in the high-margin

Face Value (`)

10

Value Added Products (VAP) segment. It is introducing many new products/

BSE Sensex

34,950

Nifty

10,524

variants of existing products like premium ghee, protein powder, Mishti Doi which

Reuters Code

PAMF.NS

would boost its revenue in coming quarters.

Bloomberg Code

PARAG.IN

Margins were decent: On the operating front, the company’s margin were robust

at 10.1% due to lower input cost which offset rise in employee and other

expenses. The company has guided for 11-12% by FY2020 on the back of

Shareholding Pattern (%)

improving product mix and distribution network.

Promoters

45.9

Outlook and Valuation: We have maintained our earnings estimates in view of

MF / Banks / Indian Fls

11.9

new products pipeline and robust H1 performance. We expect PARAG to report a

FII / NRIs / OCBs

21.2

CAGR of ~17%/35% in revenue/ earnings over FY18-20E. The stock is currently

Indian Public / Others

20.8

trading at 13.4x its FY2020 earnings, which looks attractive looking at its evolving

FMCG story. We maintain BUY with a revised target price of `330 (17x FY2020E

Abs. (%)

3m 1yr

3yr

EPS).

Sensex

(5.8)

3.9

33.3

Key Financials

PARAG

(17.9)

(7.2)

-

Y/E March (` cr)

FY2016

FY2017

FY2018E

FY2019E

FY2020E

Price Chart

Net Sales

1,645

1,731

1,986

2,271

2,706

% chg

13.9

5.2

14.8

14.3

19.2

Net Profit

49.4

35.9

89.2

115.4

162.1

% chg

33.0

(27.2)

148.1

29.4

40.5

OPM (%)

9.0

5.1

10.0

10.4

11.1

EPS (Rs)

5.9

4.3

10.6

13.7

19.3

P/E (x)

44.0

60.4

24.3

18.8

13.4

P/BV (x)

5.8

3.2

2.8

2.4

2.1

RoE (%)

13.6

5.5

12.0

13.4

15.9

RoCE (%)

15.3

4.3

15.3

17.2

20.8

Source: Company, Angel Research

EV/Sales (x)

1.6

1.3

1.1

1.0

0.8

Nidhi Agrawal

EV/EBITDA (x)

17.2

26.3

11.5

9.8

7.6

022 - 3935 7800 Ext: 6872

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Parag Milk Foods |2QFY2019 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER:

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited, Bombay

Stock Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National Commodity &

Derivatives Exchange Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and Investment Adviser with

SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a registered entity with SEBI for Research

Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number INH000000164. Angel or its associates has not

been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its

associates/analyst has not received any compensation / managed or co-managed public offering of securities of the company covered

by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Disclosure of Interest Statement

Parag Milk Foods

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or

No

relatives

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on Expected Returns:

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period)

Reduce (-5% to -15%)

Sell (< -15%)

November 6, 2018

8